Plastribution’s Polymer Price Know-How: April 2025

|

Getting your Trinity Audio player ready...

|

Plastribution’s April Polymer Price Know-How reflects ongoing uncertainty in the market, driven by the Trump Tariff Regime and fluctuating crude oil prices. Polyolefins have largely rolled over, though LLDPE and HDPE may face temporary shortages due to tariff-related disruptions. Styrene Monomer has seen a notable price drop, while engineering polymers remain under pressure amid competitive pricing challenges. The outlook for the coming months hinges on evolving trade policies, supply chain adjustments, and global economic shifts.

The Trump Tariff Regime is causing significant uncertainty across a wide range of markets, with the petrochemicals sector witnessing feedstock reductions, which correspond to both the fall in crude oil prices and to the potential demand for petrochemical feedstocks.

The initial rout has resulted in most plastic buyers adopting a ‘wait and see’ strategy as it is unclear as to whether prices will plummet, move sideways or indeed possibly move upward. Whilst no two crises are every quite the same, for many the memories of the price and availability issues are not a distant memory.

For sure there is much to be unsure of with predictions varying from non-US markets becoming awash with product as sellers are forced to seek other export opportunities for materials that that cannot overcome the high tariff hurdle, to the possibility that counter-tariffs will create import paralysis as importers avoid the risk of being caught out with material on ‘the high seas’ as punitive duties are applied.

The recently announced 90-day curfew that President Trump has granted on many of the countries and/or products facing elevated tariffs, should provide some temporary respite and alleviate the risk of counter-tariffs being imposed in the more immediate future.

For sure, the only current certainty is uncertainty, as the world waits to see the outcome of Trump Tariff Masterplan.

Monomer Price Movement

Exchange Rates

Exchange Rates

€- 1.19

$- 1.29

€/$- 1.08

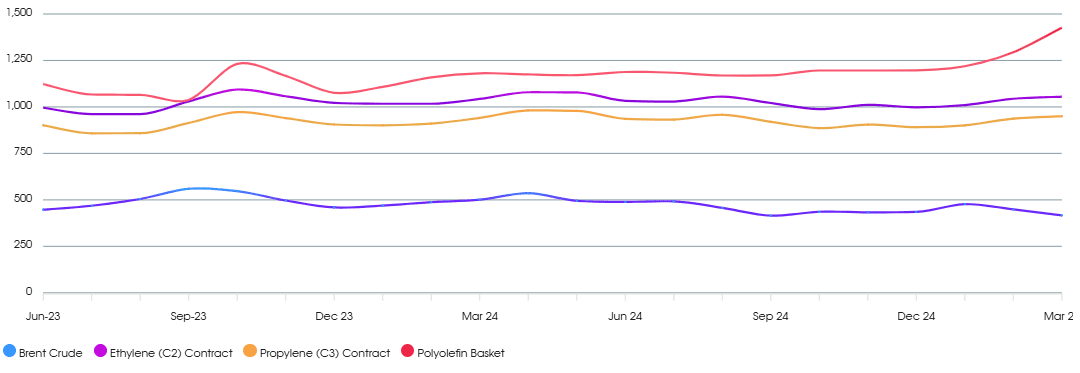

Polyolefins

April has been a month of uncertainty with markets thrown into turmoil with the announcement of tariffs, anticipation of retaliatory tariffs and the potential impact on availability and pricing of European Polyolefins.

Whilst both C2 Ethylene and C3 Propylene dropped by €55 / MT, we saw further separation in the pricing as PP typically dropped by around the monomer and PE mostly rolled over due to uncertainty surrounding availability of US imports. Whilst the tariff situation appears to have been temporarily cooled down in the last few days, it remains to be seen what impact the retaliatory tariffs from the EU the market expected to see kick in the middle of the month has had on exports from the USA. We could see a temporary shortage of the key grades we import, LLDPE and HDPE.

Outlook for the short & medium term is uncertain, and the disruption to supply chains is still not clear, but we do at least appear to have some breathing space for the next three months following the tariff suspension. With the expectation of an immediate response from the EU removed, we can expect to see stronger exports from the USA to the EU and the UK.

With the tariff uncertainty unsettling the global economy, we’ve seen oil prices fall and that is likely to be passed through into monomer pricing. Whilst the European producers are facing very challenging times, they are likely to be forced into passing reductions through as imports from lower cost regions remain strong.

The weakening £ against the € is causing some upward price adjustment requests though it remains to be seen how successful they will be in the face of poor demand

Styrenics

Contract EU Styrene falls.

Styrene Monomer has fallen by €58/T, settling at €1496/T.

For April, EU GPPS and HIPS reduced by €55-60/T and EU ABS followed (+€50/T). Non Flame retardant Import ABS Rollover. FR ABS facing increases due to FR Shortage.

GPPS/HIPS/ABS supply chains are still running at reduced rates, no doubt triggered by low demand. Converters and distributors are also running inventory at very low levels due to financial pressures. Therefore, any adjustments in polymer prices are likely to be passed on immediately.

Engineering Polymers

March ended up similar to January and February. Producers found it difficult to push through any meaningful increases in what is an incredibly competitive market with more than adequate supply. There will be renewed efforts to try again for price increases into Q2 but with the Easter holidays there could well be a distinct lack of appetite to buy.

The March benzene contract settled €179/Mt lower than February at €669/mt.

Sustainable Polymers

Recycled Polyolefins have mostly seen rollover in April but with some up and downs depending on availability and demand. PP dropped a little as demand in key sectors continues to be poor but PE did see some stronger pricing as demand picked up and there was some uncertainty surrounding the impact of tariffs on the availability of prime grades. The weakening £ against the € is causing some upward price adjustment requests though it remains to be seen how successful they will be in the face of poor demand.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE increased a little in April with some tightness in the availability of premium grades and slightly better demand as prime LDPE had been rising recently. High performance grades offering prime performance whilst meeting the requirements of the packaging tax continue to demand a strong premium over virgin grades.

Recycled HDPE

Recycled HDPE has mostly rolled over in April, the overall market is reasonably balanced with some ups and downs depending on quality and application. High quality natural grades for packaging have seen increased demand this month, some producers of high quality natural PCR HDPE are asking for prices closer to £2,000 / MT as they increased demand from major brands.

Recycled PP

Recycled PP has slightly slipped in April as prime prices are following the monomer reduction of €55 / MT and buyers are demanding similar reductions for their recycled options.

Price Know-How: April 2025 Full Report

Visit the Price Know-How website to read the April 2025 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know.

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.

+44 (0) 1530 560560

Website

Email