Plastribution’s Polymer Price Know-How: February 2025

|

Getting your Trinity Audio player ready...

|

After improved demand in January, the thoughts of standard polymer producers turned to instigating price increases for February. In the first instance, there were calls from some suppliers for ‘triple-digit’ increases, especially wherever supply was perceived to be snug for materials such as LDPE.

As the month got underway, it became clear that many converters were only prepared to accept the monomer increases and, where necessary, lived off existing inventories to put pressure on the sellers to accept more modest price rises.

Whilst far from buoyant, the overall market sentiment was more positive.

It is expected that contract monomer prices will increase again for March, and with this in mind, many polymer converters will look to maintain or increase inventory levels.

Monomer Price Movement

Exchange Rates

Exchange Rates

€- 1.19

$- 1.24

€/$- 1.04

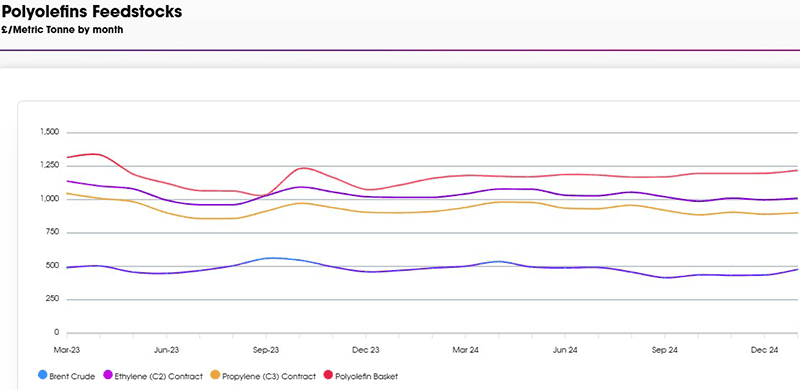

Polyolefins

February has seen the first significant price movement in months, with relatively big increases in monomer passing through, and for some grades, significant premiums above monomer have been reported. Both Ethylene C2 and Propylene C3 were late settling, with much disagreement between buyers and sellers.

C2 eventually settled at +€55 / MT, with C3 just behind at €52.50 / MT. Whilst increased Naphtha costs were cited as one reason, the monomer producers are also concerned about increased production costs and with some planned and unplanned shutdowns of capacity in Europe, sellers had a slightly stronger hand.

LDPE has seen the biggest increases of around €100 / MT as suppliers looked to balance output with demand that was much stronger in January as buyers looked to replenish stocks. Import grades such as HDPE and LLDPE mostly saw monomer increases, though some looked to recover a little of the lost margin of last year with requests for €70-80 / MT increases.

Polypropylene generally saw increases in line with monomer, but there were some attempts at increases above this. Positions varied depending on whether a supplier was looking to improve market share or to improve margins that were heavily impacted towards the end of last year.

The outlook for the short term is for potential small increases in March before some stability in April. Early suggestions are for slight (€10-20 / MT) increases in monomer in March, and this is likely to be passed through. We are, however, facing some uncertainty with global trade, potentially facing the impact of tariffs that could be implemented at short notice. It remains to be seen how much this may impact imports and exports of PE and PP, that are truly global products. Whilst they are both currently in a global oversupply situation, we may have a bumpy road in terms of supply chain if traditional export routes are disrupted.

The European Petrochemicals Industry is in a very “Dynamic” period with many rumours surrounding further limits to production with temporary shutdowns and possible permanent closures of assets. We should see further announcements in the coming months.

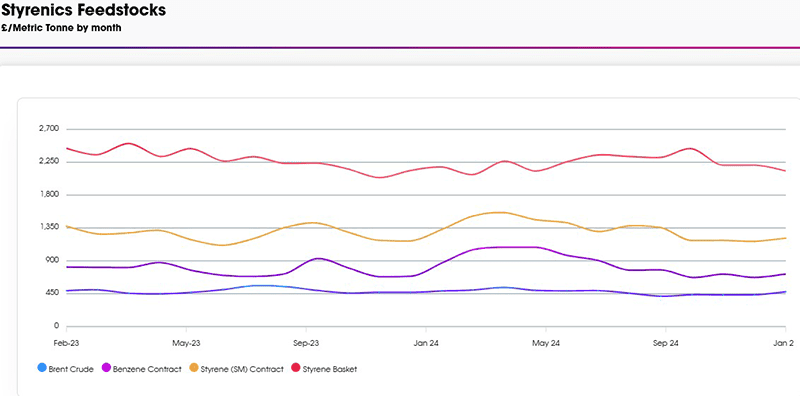

Styrenics

Contract EU Styrene rises again.

Styrene Monomer has increased by €45/T, settling at €1489/T.

For February, EU GPPS and HIPS increased by €45/T, and ABS followed.

GPPS/HIPS/ABS supply chains are still running at reduced rates, no doubt triggered by low demand. Converters and distributors are also running inventory at very low levels due to financial pressures. Therefore, any adjustments in polymer prices are likely to be passed on immediately.

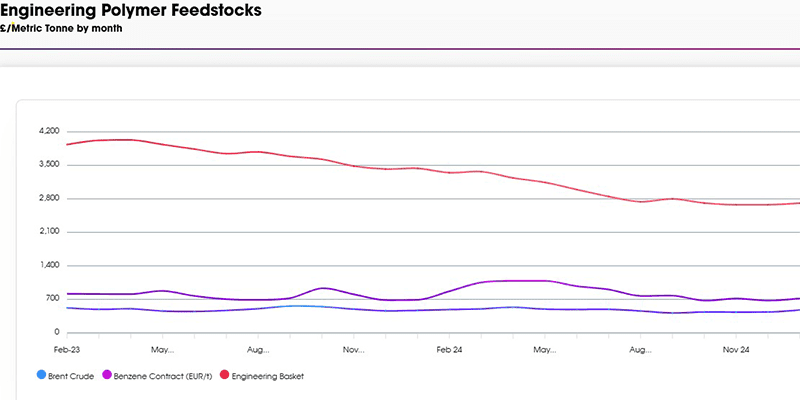

Engineering Polymers

January saw a slight uplift in order activity, in part due to a shorter trading month in December, where many moulders finished early for the Christmas break. It looks unlikely that there will be any notable changes to demand, supply, or prices in February.

The February benzene contract settled €2/Mt higher than January at €859/Mt.

Sustainable Polymers

Recycled Polyolefins have seen some strengthening in February on the back of decent increases in virgin prices. Most of the increases have been felt at the lower end of the market, where struggling producers of recyclate have finally been able to pass through some much-needed increases, though it is still a struggle to make some grades profitably.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE has increased in February around £30-50 / MT as virgin PE saw strong increases.

Whilst demand is not strong, recyclers see an opportunity to raise prices for those that use recycled as a substitute for cost reasons.

Recycled HDPE

Recycled HDPE saw increases of around £30-50 / MT as virgin PE saw stronger pricing. Some demand pick up in markets such as construction was seen.

Some reports that pricing for the high-quality natural grades used in consumer packaging were seeing a plateau as demand was no longer increasing beyond supply.

Recycled PP

Recycled PP has seen slight increases of around £30-50 / MT as virgin prices have increased. As with HDPE, the high quality natural grades for consumer packaging are also seeing a price plateau though still at a significant premium over virgin.

Price Know-How: February 2025 Full Report

Visit the Price Know-How website to read the February 2025 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know.

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.

+44 (0) 1530 560560

Website

Email