Plastribution’s Polymer Price Know-How: 2023 Review

|

Getting your Trinity Audio player ready...

|

Despite the challenges of 2023, the UK plastics sector has once again demonstrated resilience in the face of significant challenges.

UK Economy, Brexit, and Post-COVID 19 Pandemic

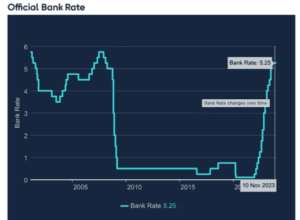

Contrary to the expectations of many economists, the UK avoided recession in 2023, and modest growth was reported. Inflation was a dominant issue, with RPI and CPI peaking above 10% before moderating towards the end of the year.

For plastic converters, the falling cost of raw material inputs mitigated the impact of inflation. Interest costs have peaked at a 5.25% Bank of England rate. There is evidence of lenders in the domestic mortgage sector becoming more competitive to secure business.

Logistics

Since the extreme inflation in East-West container shipping rates peaked in mid-2022, prices fell back to more than expected in 2023, as illustrated in the table below. High shipping costs in typical polymer prices can become prohibitive for raw material imports. They can become a barrier from the perspective of importing more competitively priced polymers from other regions of the world.

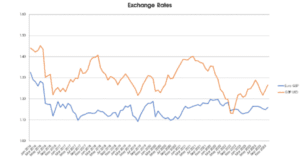

Following the short-lived Liz Truss premiership and the ensuing Kwasi Kwarteng autumn statement/’mini budget back in 2022, the value of the GBP has recovered significantly, achieving a reasonable level of stability against the Euro and gains against a slightly weaker USD.

The result of the June 2016 Brexit referendum has permanently impacted the value of the GBP, with the value against the Euro dropping from the 1.30’s to the 1.10’s. The USD turbulence is more related to political and economic developments within and outside the US.

Crude Oil

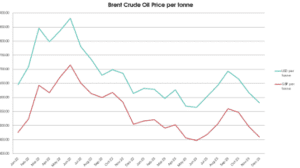

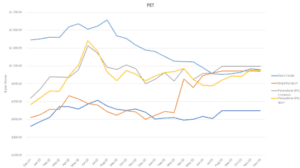

Brent Crude traded in a relatively tight range of 75 – 90 USD per barrel. Prices fell until mid-2023 before a short rally over the summer months and then fell sharply back to levels that were below those at the start of the year.

Feedstock

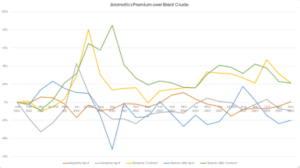

The volatility of aromatic feedstock continued in 2023, with both Benzene and Styrene monomers recording significant swings, often independent of Brent Crude and Naphtha. The olefin situation was dominated by over-supply, with spot prices trading at a substantial discount to the contract values.

In the case of C2, high import penetration of competitively priced PE suppressed demand. Although C3 is typically a coproduct of Naphtha cracking from C2 production, the reduction was insufficient to avoid a glut of C3 and, hence, the significant discounts for spot purchases.

PVC – Suspension & Emulsion

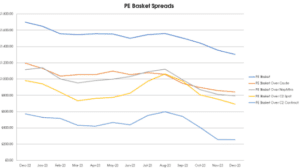

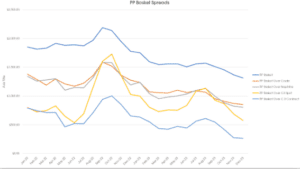

Polyolefins

With the exception of a couple of minor upward blips in April and November, the price trend was fundamentally downward for the polyolefins basket. Polymer converters were able to exploit the intense competition among suppliers to their advantage.

Polypropylene and polyethene pricing coincided by the end of Q1 2023, and this is due to several factors, including:

- A relative reduction in the C3 price compared to the C2 price

- PP producers taking advantage of the low C3 spot pricing

- Lower production and demand for consumer durables such as cars and white goods, for which PP is a much more significant market segment than PE.

The supply of PE from the USA that resumed in 2022 became a dominant factor in 2023, with a strong flow of materials for film extrusion and blow moulding arriving at competitive prices. UK converters have become accustomed to the longer lead times and consequently need to make forward price commitments often to secure supply.

Styrenics

Engineering Polymers

The engineering polymers market reflected the broader global economic situation, with prices sliding throughout the period. The high level of competition for available volumes eroded producer margins.

The UK General Election, likely to be held in the second half of the year, will be a significant factor affecting the UK economy, before which a budget in March may offer some economic stimulus through lower taxation rates at either a personal or corporate level. Forecasts from the UK manufacturing sector are robust, with growth anticipated. Some recovery in the consumption of consumer durables is likely as consumer behaviour returns to a more normal pattern.

The UK Government continues to review the UK REACh legislation and has already extended the registration deadlines. Consultation that took place in 2023 may result in further changes, and it is anticipated that registration fees are set to be lowered.

Logistics

Please click here to subscribe for free and receive monthly updates directly to your inbox.

To read more on Plastribution click here.