Polymer Price Know-How: September 2023

|

Getting your Trinity Audio player ready...

|

The leading polymer distributor, Plastribution, has released the latest instalment of Price Know-How. Price Know-How helps plastic raw material buyers make informed purchasing decisions. This month, the market reacts to the widely-anticipated increase in contract monomer pricing, with many polymer converters having already increased inventories to resist accepting the price hikes.

Overview: September 2023

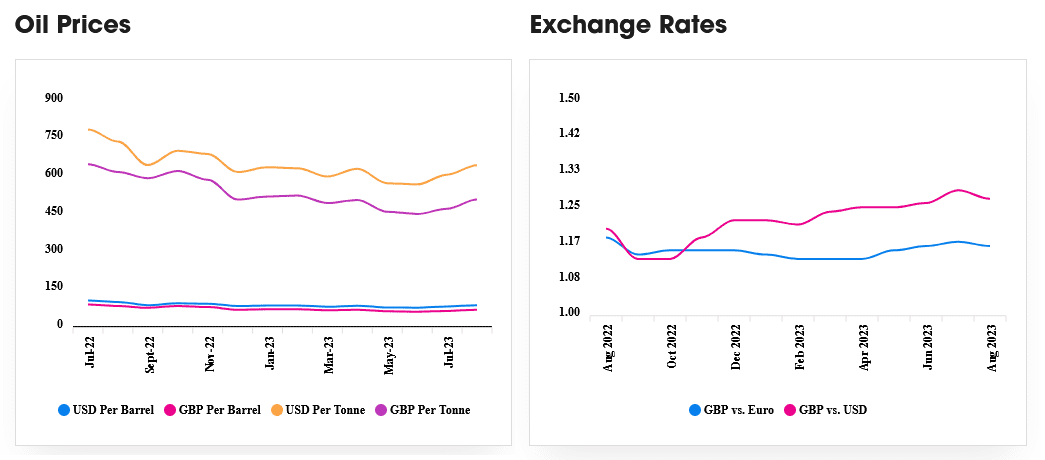

How will the market react to feedstock price inflation?

The situation for more specialised materials continues to be rather weak, with sellers chasing available business and competing for market share. Some recovery in demand for mobility/automotive applications has not been matched with increased demand in the consumable durables and construction sectors and hence the on-going weak demand overall.

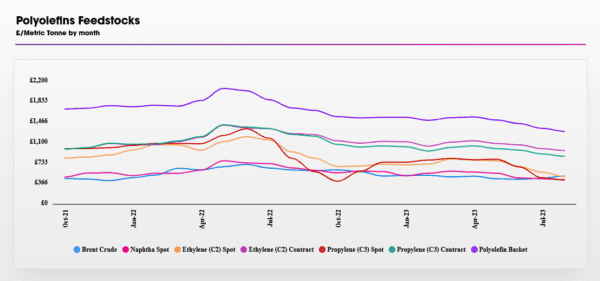

Polyolefins

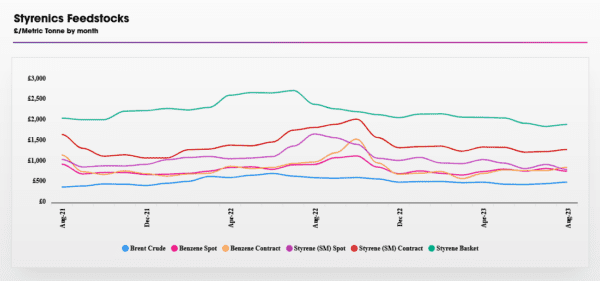

Styrenics

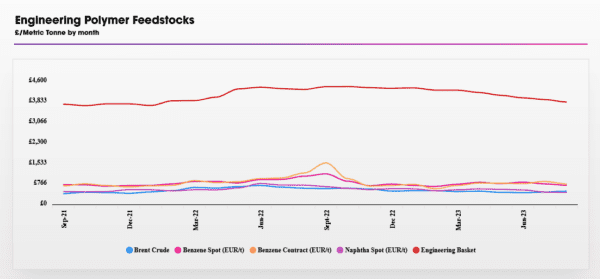

Engineering Polymers

Price Know-How: September 2023 Full Report

Visit the Price Know-How website to read the September 2023 update, including an in-depth analysis of each market segment and material group by Plastribution’s expert product managers.

Subscribe and keep in the know.

Price Know-How is an industry-leading report to keep you updated on polymer pricing and market fluctuations. A trusted, go-to resource for over a decade, Price Know-how is produced by the thermoplastics experts at the leading polymer distributor, Plastribution, with data from Plastics Information Europe.

Unlike many pricing reports, Price Know-How is tailored specifically for the UK polymer industry. We do all the currency conversions, so you don’t need to!

To subscribe for free and receive monthly updates directly to your inbox please click here.