Plastribution’s Polymer Price Know-How: September 2025

|

Getting your Trinity Audio player ready...

|

Plastribution’s September Polymer Price Know-How highlights continued weakness across the polymer market, as subdued summer sentiment rolls into autumn. Despite a small increase in ethylene and a propylene rollover, falling feedstock and crude oil prices have reinforced downward pressure on polymer prices. UK manufacturing output remains low, imports remain high, and demand continues to lag across most sectors. With no major shift expected in the short term, the market outlook remains flat, and buyers retain the upper hand in pricing negotiations.

Whilst the months of July and August are typically quiet in Western Europe as seasonal holidays take effect, this summer appeared to be quieter than ever with sellers perhaps trying to avoid conversations with buyers as availability across most polymer grades only appeared to increase.

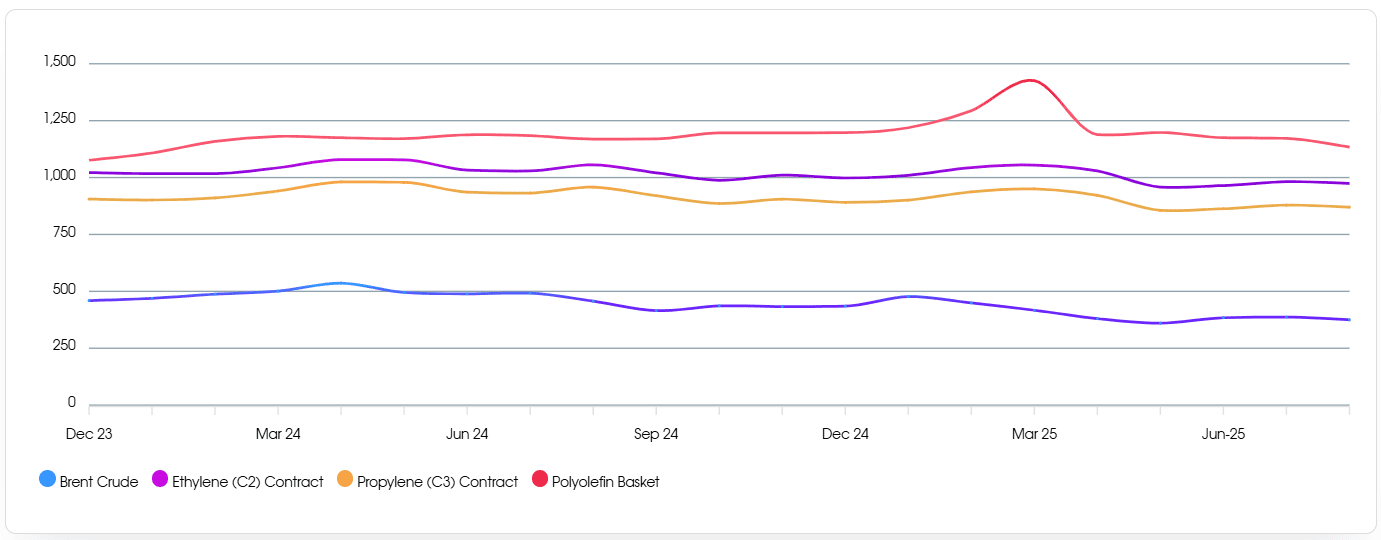

Monomer Price Movement

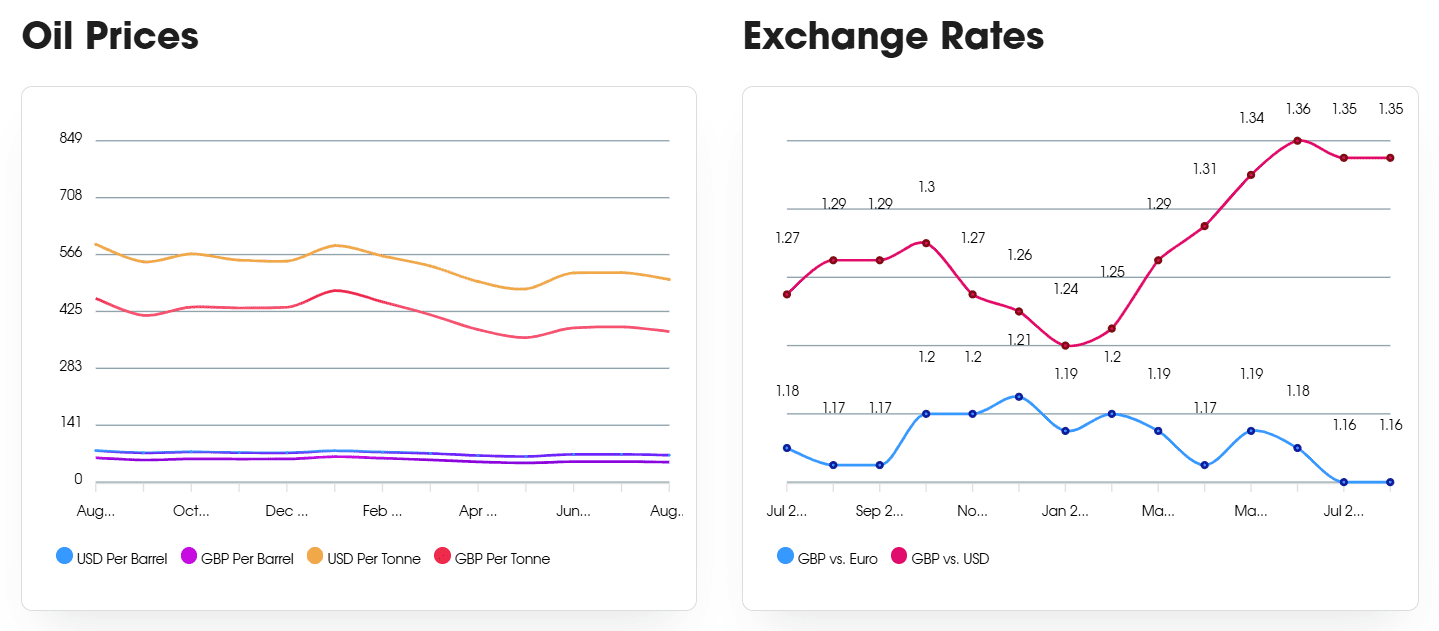

Exchange Rates

€ – 1.16

$ – 1.35

€/$ – 1.17

Standard Polymers

September appears to be seeing reductions in both PE and PP. Although Ethylene increased €5 / MT and Propylene rolled over, there is simply too much material available in the market and nowhere near enough demand to absorb it. The supply and demand dynamic is beating the cost pressures that the producers are facing. Although European producers are deeply in the red with margins, the level of imports continues to be significant, and prices are reflecting this with buyers holding a strong bargaining position.

Talk of rationalisation within the European Petrochemical industry continues with the announcement of a likely 0% tariff on imports of polymers from the USA doing nothing to ease concerns about the profitability of aging plants. Whilst the “market price is the market price” still holds true whether tariffs are applicable, without a shift in demand, the writing is very much on the wall for European production of commoditised grades. The only hope appears to be finding niche applications for high performance grades in Metallocenes and Impact Copolymers.

Outlook for the coming months is largely expected to be flat as there is little indication of a change in market conditions.

Polyolefins Feedstocks

Performance Polymers

The UK market for performance polymers continues to be very subdued, with low demand, and high stock levels. Imports from Asia remain high, and as a result of these factors, many European producers continue to cut production during the holiday period. There was renewed efforts by some manufacturers to try and push small price increases through, however with the ongoing weak demand and the global oversupply situation, most polymer costs actually softened yet again.

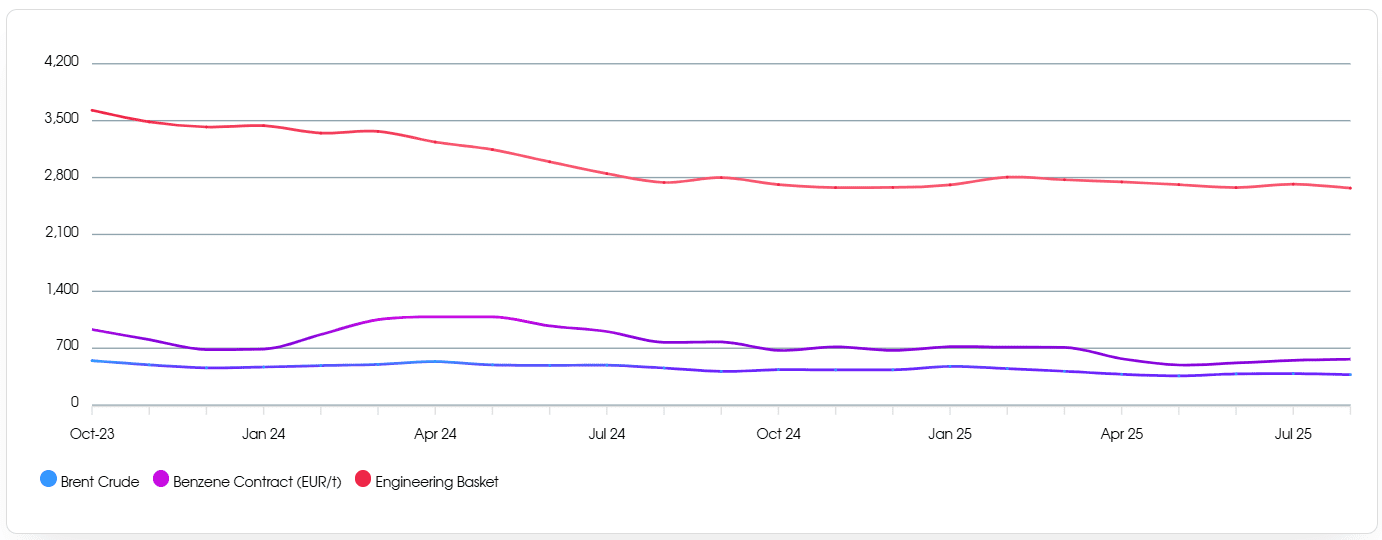

The August benzene contract settled at €653/t, an increase of €16/t from July, whilst September sees a decrease of €75/t, with the price settling at €578/t.

Engineering Polymer Feedstocks

Sustainable Polymers

Recycled Polyolefins has largely seen a rollover in September as there appears to be no further room for reductions on prices that are typically below the cost of production for many recyclers. However, with virgin prices dropping, some of the small increases that were secured in August appear to have been lost. Demand is weak and although some recycling facilities in the UK have closed, there is still very good availability.

Recycled LDPE / LLDPE

Some grades are slipping, some higher quality grades are staying stronger on pricing.

Recycled PP

Typically a rollover in September, but some suppliers are looking at deals to move volume in the face of continued weak demand.

Recycled HDPE

Recycled HDPE has typically rolled over in September, demand remains weak, and this may have some impact on pricing.

Price Know-How: September 2025 Full Report

Visit the Price Know-How website to read the September 2025 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.