Plastribution’s Polymer Price Know-How: July 2026

|

Getting your Trinity Audio player ready...

|

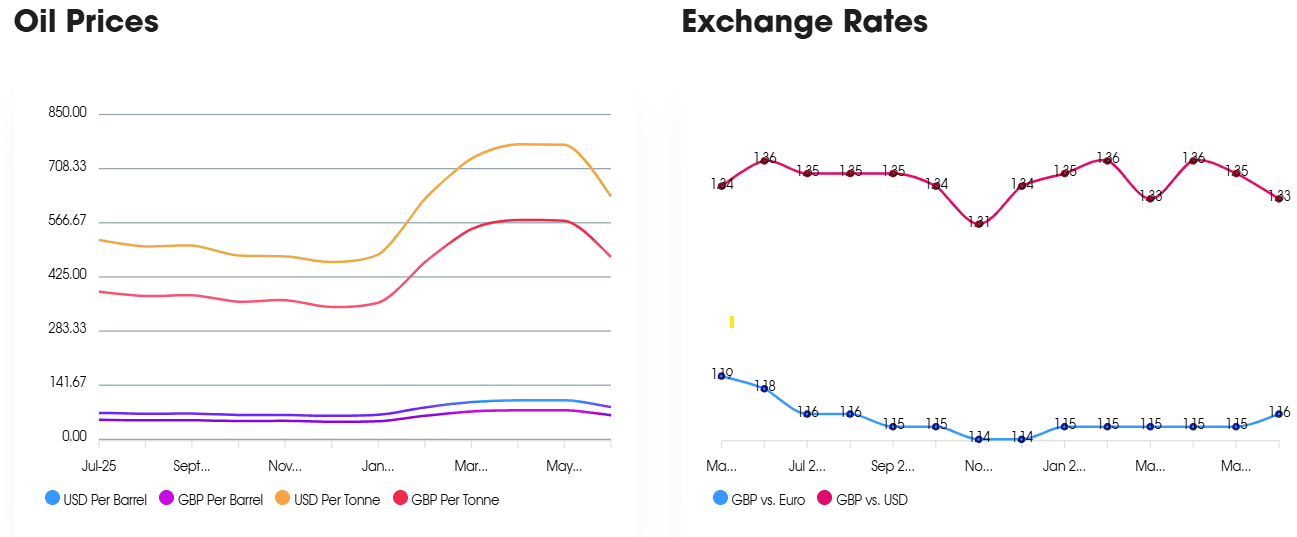

In the July Price Know‑How, Plastribution reports that polymer markets continue to soften despite firmer crude oil values. Even with Brent averaging just above $100 per barrel, PE and PP prices have fallen sharply as the surge in stock‑building earlier in the year left converters with limited requirements. The easing of US–Iran hostilities and the reopening of supply routes have removed much of the upward pressure seen in April and May, and with seasonal shutdowns now underway across Western Europe, demand remains muted.

Prior to the start of the US/Iran conflict, market price action was dominated by plentiful supply in a market with lacklustre demand.

The impact of the conflict and, in particular, the closure of the Strait of Hormuz, drove the buyers of standard polymers to secure inventory, and whilst demand appeared to exceed supply, prices skyrocketed in April and May.

For PE and PP, June prices fell away quickly as the hostilities eased and market fundamentals returned to their pre-conflict status. For most players, there is no reason, apart from slightly higher crude oil prices, why prices should not return to the levels seen in January and February of this year.

Whilst a few issues remain on some raw materials such as pigments and additives, performance polymers barely have had time to react before the situation in the Middle East eased, pricing of engineering plastics has barely changed.

Demand over the months of July and August is typically low, as many converters in Western Europe take seasonal holidays and enjoy factory shutdowns.

Although demand will likely improve in September, the situation of bountiful supply is likely to remain throughout the remainder of 2026.

Exchange Rates

€ – 1.16

$ – 1.33

€/$ – 1.16

Standard Polymers

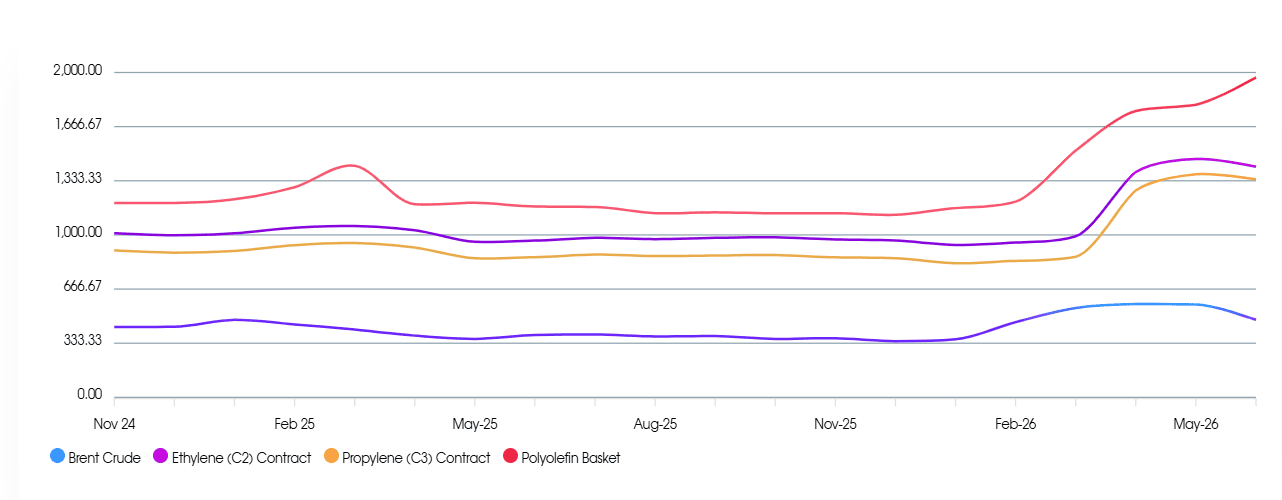

July has seen further significant price reductions for both PE and PP, as the market continues to find a new level following the volatile pricing of recent months. Monomers C2 and C3 dropped by €200 and €190 / MT respectively.

The July price drop depends on your starting point. We saw price erosion through the month of June, with prices at the end of the month around £250 / MT lower than at the start. July pricing from the start of June is around £400 / MT lower for most grades of PE and PP when compared to the start of June.

At the time of writing, oil pricing was up as the ceasefire in the Middle East has appeared to have failed. However, the market is not reacting as it did before and there doesn’t appear to be any significant panic.

Whilst a price rebound seems unlikely, it should put a brake on the price reductions as buyers return to the market and start securing safety stocks rather than a just in time approach.

Polyolefins Feedstock

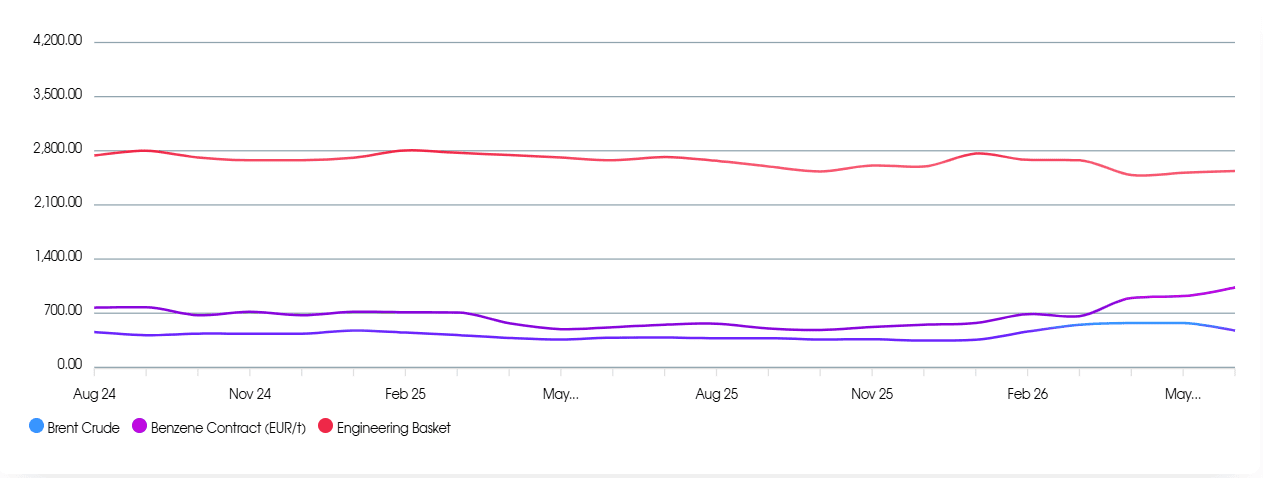

Performance Polymers

It is still very much a mixed market, with some renewed volatility due to increasing tensions between Iran and the US, but demand is subdued as the traditional summer holiday period gets underway.

Prices appeared to have bottomed out in June and the market was showing signs of cost reductions, but this latest news and the increase in the oil price may change the situation yet again.

The benzene contract price for July settled at €1,093/t, down by €102/t from June. Availability was improved as demand has fallen.

Sustainable Polymers

Recycled Polyolefins have fallen in July as virgin prices dropped significantly and put pressure on suppliers. Demand remains muted and those that switched from virgin to recycled as virgin prices soared in March and April are returning to virgin.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE has dropped triple digits as demand has slumped. Recyclers were optimistic as demand had a mini boom with the sudden virgin price increases of March and April, but this has been short lived.

Whilst high quality grades continue to command a premium over virgin to meet the needs of packaging tax, low quality grades are under pressure again.

Recycled HDPE

Recycled HDPE is dropping as virgin prices have dropped and availability is no longer an issue.

Natural grades are still in demand for consumer goods with Sustainability credentials but industrial grades for use in construction etc. are struggling to find buyers as demand is weak.

Recycled PP

Recycled PP is dropping triple digits. Natural pricing is relatively strong but industrial grades are readily available and demand is not great.

Price Know-How: July 2026 Full Report

Visit the Price Know-How website to read the July 2026 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.

+44 (0) 1530 560560

Website

Email