Plastribution’s Polymer Price Know-How: March 2026

|

Getting your Trinity Audio player ready...

|

In the March Price Know How, Plastribution reports rising polymer pricing as geopolitical tensions in the Middle East dramatically affect the global supply chains. With shipping routes disrupted and regional petrochemical infrastructure under attack, materials are now facing rapid price escalation, tightening availability, and a market gripped by uncertainty.

The military action taken by the United States and its allies against Iran has pushed polymer pricing into hyperdrive, as the market starts to comprehend the disruption that is now ensuing.

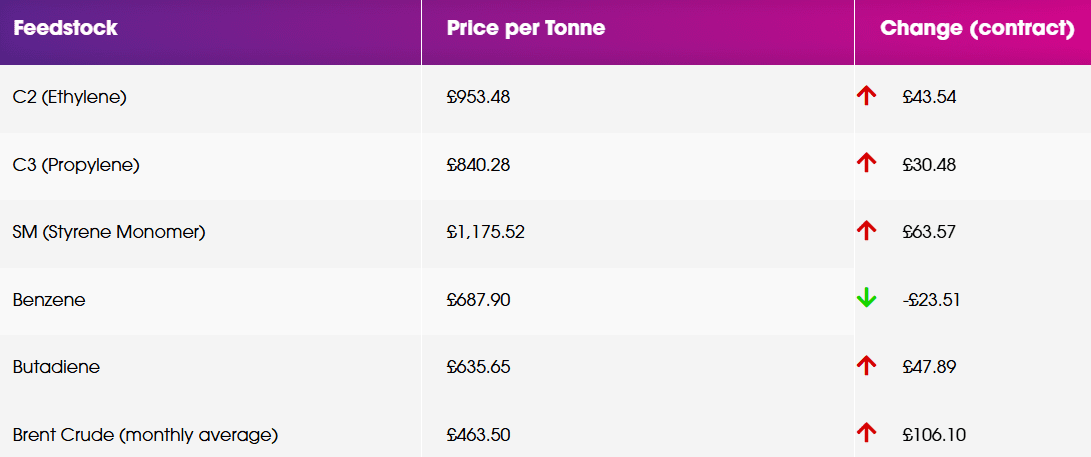

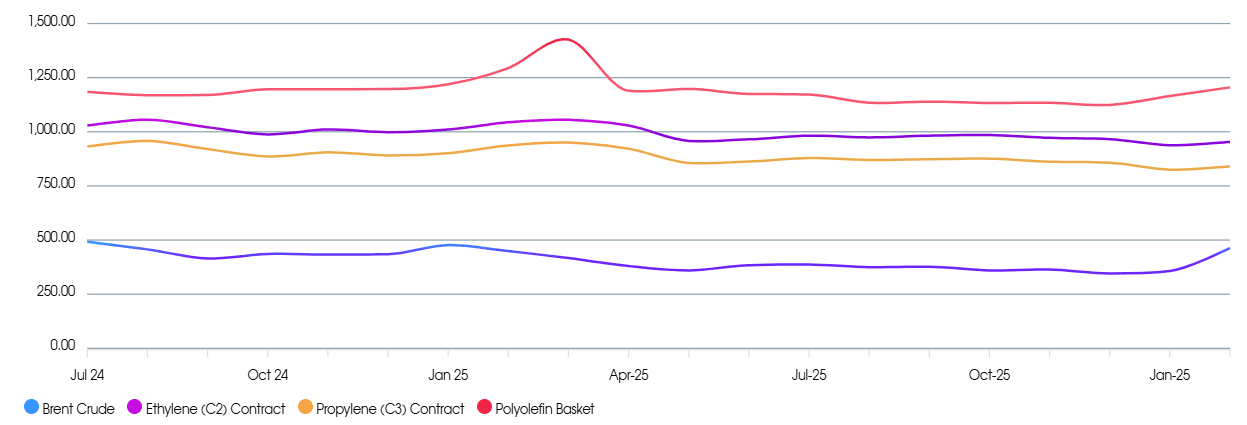

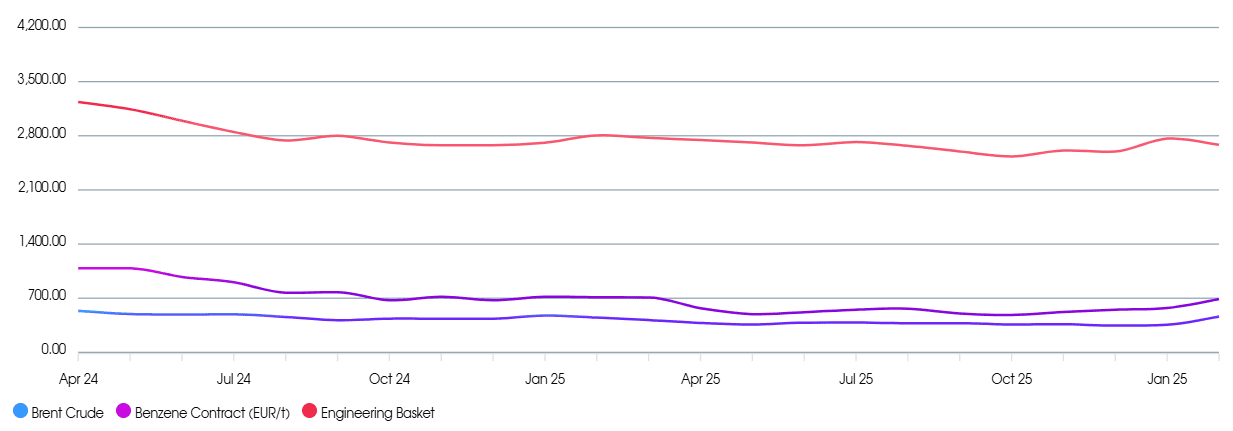

Whilst the C3 propylene contract in Europe for March settled at +€35 per tonne on the Friday before the conflict started, the C2 ethylene settled after the hostilities got underway and recorded a more significant +€50 per tonne increase, the reaction of polymer prices has been significantly inflated.

In the case of PE many suppliers March started with +€200 per tonne; a request which initially met with incredulity, but as the reality of shipments not being able to pass through The Strait of Hormuz, and Iranian attacks on the refining and petrochemical facilities of its neighbours dawned, so the prospect of supply shortages for plastic converters became a reality, and what at first looked expensive, soon became more reasonable as price levels have increased further and announcements of restrictions abound.

Even if the conflict is resolved quickly, the repercussions in the supply chain are likely to be felt for many months to come and even though the polymer market fundamentals remain as a situation of over-supply, for now, material is hard to get hold of and in high demand. The inevitable result is higher prices and a requirement for significant due diligence to confirm availability wherever material is currently in transit.

Monomer Price Movement

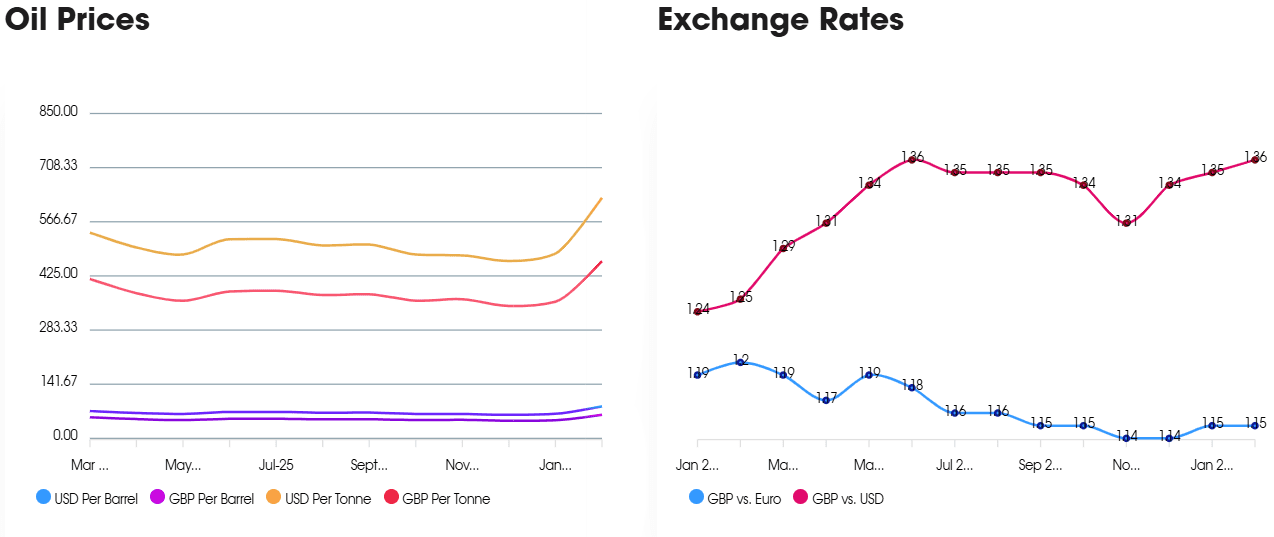

Exchange Rates

€ – 1.15

$ – 1.36

€/$ – 1.18

Standard Polymers

This is a very challenging and dynamic situation following the escalation of the conflict in the Middle East. Whilst at the time of writing, the prices for PE and PP appear to be increasing in the region of €200-300 / MT, we are seeing prices moving on a daily basis, and this may not be accurate for long. There are rumours of planned increases in excess of €500 / MT due to significant uncertainty around material replenishment. Many suppliers in Europe have either declared Force Majeure on supply or are on order stop.

We are dependent on the Middle East for imports of both PE and PP, and whilst there are options of securing PE from USA sources, many other regions will be looking for product, and they will sell to the highest bidder. PP is less easy to replace, and as Asian producers rely on Middle East Naphtha for their crackers, they will not be able to fill the gap.

C2 Ethylene rose by €50 / MT and C3 Propylene rose by €35 / MT, but these are not that relevant this month, considering the supply chain disruption.

Polystyrene has increased above the monomer rise of €73 / MT. Whilst the supply concerns are not as great as with PE and PP, Europe imports styrene monomer from the Middle East, and availability could tighten quickly. Increases of €150-200 / MT are being reported.

Prices are expected to further strengthen in the coming months until there is more clarity on how material will get to Europe and the UK. Presently, securing sufficient material is of greater concern than what it costs. Even if the conflict is resolved quickly, it will be many months before the supply chain returns to anything like normality.

Performance Polymers

The current situation is dominated by events in the Middle East. It remains to be seen just how much of a medium to long-term impact it will have, but for now, the messaging is one of higher prices, longer lead-times, shipping issues and general delays.

Some producers have introduced temporary surcharges, whilst others have stopped accepting orders altogether. With prices already on an upward curve, the events of recent times will only increase the momentum for higher prices, while, simultaneously, inventories will start to be depleted.

The Benzene contract price in March settled at €763/t, down by €27/t from February, but this is now completely irrelevant due to events in the Middle East.

Sustainable Polymers

Recycled Polyolefins are starting to see prices recover as the impacts of the Middle East conflict are felt throughout the industry. With very significant price increases and restricted availability of prime materials, buyers look to recycled options more, and we can expect to see demand for recycled grades outstrip supply.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE has seen some increases in March, absolute levels are hard to pick due to the range of quality and specification, but with prime LDPE and LLDPE up by £200+ / MT. We can expect to see triple-digit increases soon.

Recycled HDPE

Recycled PP should see strong increases in the coming months as prime PP hits a big supply crunch. The Middle East is a big supplier of PP to Europe, and with shortages expected in the coming months, recycled PP is more likely to be substituted in.

Recycled PP

Recycled PP is increasing slightly or rolling over, depending on the starting point and the quality of the grade. Demand is up a little, but it remains a challenging market.

Price Know-How: March 2026 Full Report

Visit the Price Know-How website to read the March 2026 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.

+44 (0) 1530 560560

Website

Email