Plastribution’s Polymer Price Know-How: April 2026

|

Getting your Trinity Audio player ready...

|

In the April Price Know‑How, Plastribution reports a market under extreme pressure as polymer prices surge far beyond monomer movements, driven by severe supply disruption across the Middle East and the resulting blockade of the Strait of Hormuz. With crude oil and natural gas costs rising, petrochemical plants damaged or starved of feedstock, and inventories rapidly depleting, availability has tightened at a pace not seen since the post‑pandemic period. With uncertainty surrounding the duration of hostilities, the timeline for plant repairs, and the recovery of global shipping, April emerges as a defining moment for UK polymer pricing.

Concerns over the supply situation have caused rapid price inflation for all polymers, with standard polymers, including polyethylene and polypropene, experiencing the most violent price movements as concerns about availability drive market dynamics.

These pressures are multifactorial and include increased crude oil and natural gas costs, damage to petrochemical plants across the Middle East, petrochemical plants in South-East Asia starved of feedstock, and inventories of polymer being marooned as a result of the Iranian blockade affecting shipments through the Strait of Hormoz. Probably, the full extent of supply outages is yet to be realised until existing supply chains have fully emptied; after all, just a few weeks ago, there were global surpluses of almost all polymers, with local warehouses and supply lines with bountiful products.

In many cases, prices have already risen to levels above those witnessed in the immediate aftermath of the Covid-19 pandemic and the subsequent Russian invasion of Ukraine.

What is still entirely unclear is, when hostilities will diminish to enable normal trade, how long it may take to repair damaged petrochemical complexes, how long it will take for global shipping to return to normal and what impact there may have been to underlying demand (as and if either consumers stop buying plastics related products or if plastics are substituted by cheaper and more available alternatives).

The fundamentals of supply and demand economics do have limits that are determined by the market, although this can be complex in products such as packaging, where a drastic increase in the plastics element will not necessarily result in such a significant % price change for the product. That said, there appears to be some evidence of prices peaking as suppliers start to moderate their approach

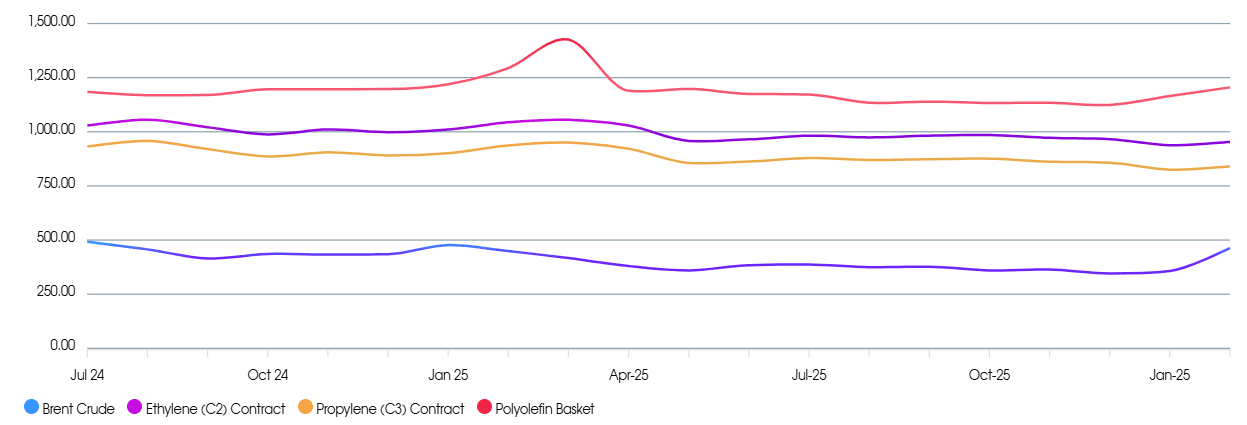

Monomer Price Movement

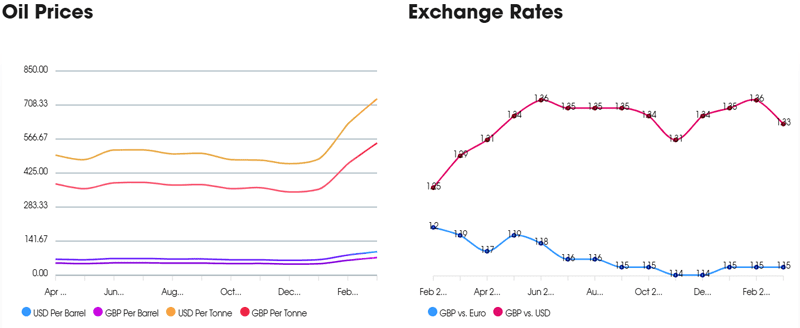

Exchange Rates

€ – 1.15

$ – 1.33

€/$ – 1.17

Standard Polymers

April has seen significant increases in all polymers as we face a severe crisis in availability throughout the supply chain of polymers due to the disruption in the Middle East, particularly the lack of transit through the Strait of Hormuz.

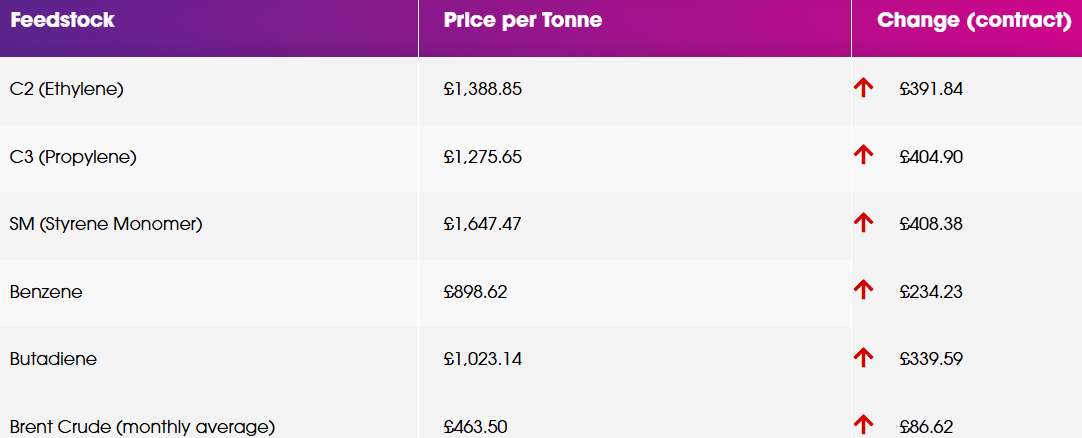

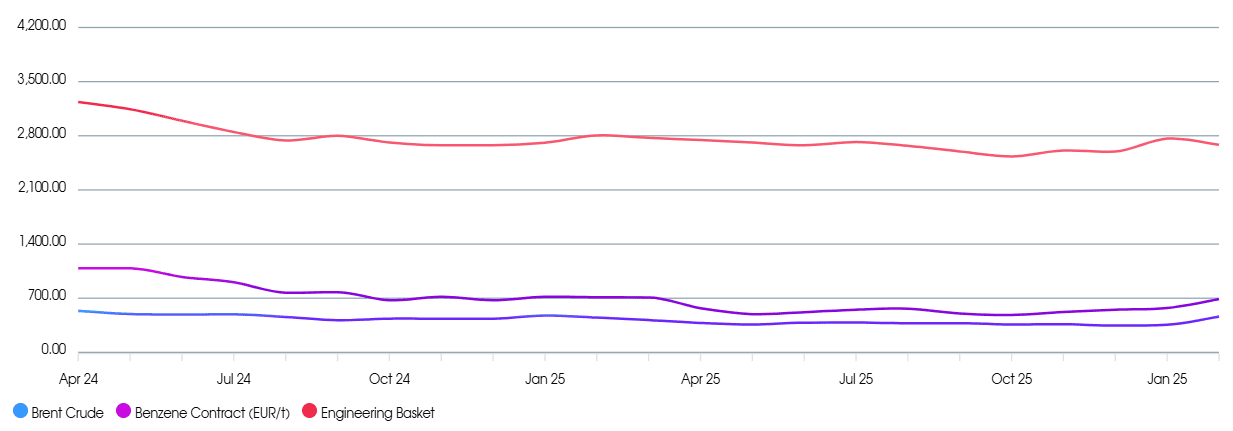

Both C2 and C3 monomer contract prices have risen by record amounts, C2 by €450 / MT and C3 by €465. In total, over the 2 months since February, both are up €500 / MT. Spot prices for C2 and C3 are trading above the contract price. This is driven by the lack of availability and the cost of Naphtha. Styrene Monomer is up €469 / MT over March.

The price increases we are seeing in April for PE and PP over the price we had in February are at least €1,000 / MT. For some materials in particular, short supply and high demand, the increases are reported around €1,500 / MT.

Many are asking why the increases are so far above the movement in monomer and the answer is that the price is driven by supply and demand. For much of 2025, European producers were selling PE and PP at a loss with the gap from monomer to polymer less than the cost of production. With the change in the market, they are looking to recover to a position where it is profitable to make polymers again.

Performance Polymers

The market situation is still being dominated by events in the Middle East. It remains to be seen just how much of a medium to long term impact it will have, but for now, the messaging is one of higher prices, longer lead times, shipping issues, and general delays.

Some producers have introduced temporary surcharges, whilst others have stopped accepting orders altogether. With prices increasing rapidly and by large amounts, the events of recent times will only increase the momentum for higher prices, while simultaneously, inventories are being depleted.

The Benzene contract price for April settled at €1032/t, up by €269/t from March, with availability also severely impacted.

Sustainable Polymers

Recycled Polyolefins are starting to see significant price increases as demand surges. With virgin prices up significantly and availability restricted, many buyers are turning to recycled material to fill the gap. Increases of €200-300 / MT are being reported, particularly for the higher quality grades that can more easily swapped in for virgin.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE has seen some very strong increases in April, higher quality grades are up €300-400 / MT as buyers look for alternatives. The more industrial grades are also seeing healthy increases in the region of €200 / MT as demand outstrips supply. Recyclers will also be looking to pass on the much higher costs of inputs as bale prices for scrap are now reported well over £1,000 / MT for high-quality sources.

Recycled HDPE

Recycled HDPE has up sharply in April with increases of €150-300 / MT reported depending on the starting point and the quality of the product. As with LDPE, demand for grades that can be swapped into virgin applications is very strong, whilst industrial grades are seeing more modest increases, they are still up to highs not seen for many years.

Recycled PP

Recycled PP is also seeing big increases as virgin PP becomes very tight. Increases of €200-300 / MT are widely reported.

Price Know-How: April 2026 Full Report

Visit the Price Know-How website to read the April 2026 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.

+44 (0) 1530 560560

Website

Email