Plastribution’s Polymer Price Know-How: February 2026

|

Getting your Trinity Audio player ready...

|

In the February Price Know How, Plastribution highlights a market under pressure as polymer producers push for increases beyond contract feedstock movements, despite demand remaining subdued. Tight LDPE supply, rising benzene and styrene costs, and early signs of firmer pricing across PE and PS are shaping a month that could set the tone for the first half of 2026. With converters resisting hikes and global factors adding volatility, February emerges as a pivotal moment for UK polymer pricing.

It is difficult not to notice the financial plight of global polymer producers, with further announcements of losses, closures, sales of non-performing assets and job cuts, and now it looks as if producers are taking the bold step of increasing prices in a market that is not necessarily demand-led.

Notifications of +50€ / £43 per tonne from some producers for many PE grades were not well received with converters, and in response, concessions have been made with typically about half of this hike currently being applied to LLDPE and HDPE. LDPE was an exception, and tight supply has enabled producers to adopt a more robust approach. The concessions will likely prove prudent as converter demand is likely to remain stable, rather than significantly diminished by buyers who elect to draw their requirements from inventory in protest..

The hefty Benzene and SM costs will also result in some hefty increases for derivative polymers.

Whilst February is a short month, it will likely be defining in terms of the first half of the year and given the economics of producers, there is likely to be a further push towards higher prices which no doubt will meet with resistance from plastic processors.

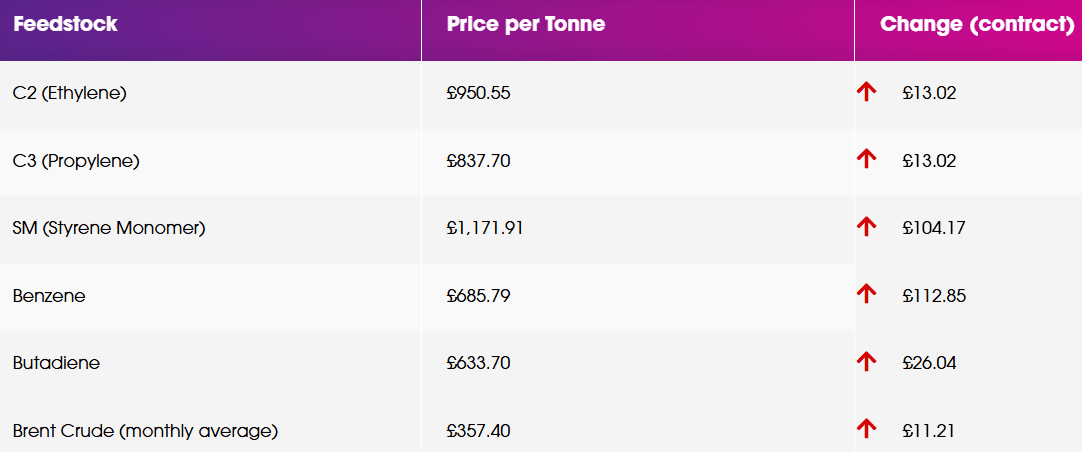

Monomer Price Movement

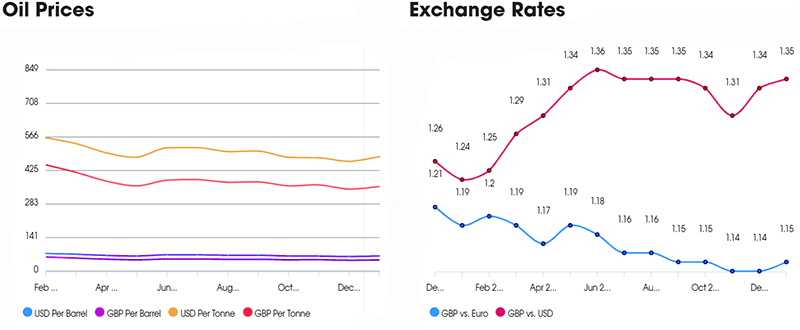

Exchange Rates

€ – 1.15

$ – 1.35

€/$ – 1.17

Standard Polymers

February has seen a general uptick in pricing on the back of monomer increases of €15 / MT for both Ethylene and Propylene. Increases vary from the monomer increase to +€50 depending on the product and the starting point. LDPE continues to show strength due to SABIC FM and restricted availability in Europe and is at the top end of these price increases.

The rest of the PE family has also gone with more than monomer and HDPE Injection appears to be a little bit tight and has gained almost as much. HDPE Blow Moulding & Film and LLDPE are showing more modest increases of around €25 / MT.

PP continues to be a little bit weaker than PE but on the back of a rollover in January it is continuing a slight price recovery in February around the monomer increase.

Polystyrene has seen a big increase of €120 / MT on the back of the monomer surprising many with a substantial increase.

Prices are expected to stay relatively strong in the coming months. Spot naphtha is trading at the highest level for 4-5 months and exporters of PE from USA are looking to raise their prices as they see stronger domestic pricing. We’re also in turnaround season in Europe with many plants undergoing scheduled maintenance between now and May. Market is expected to be a little tighter and there is hope that we will see some recovery in the manufacturing sector driving a demand improvement.

Performance Polymers

February has brought quite a few price increase announcements, but it remains to be seen how successful these will be, as the market is still subdued with weak demand, high inventories & good availability.

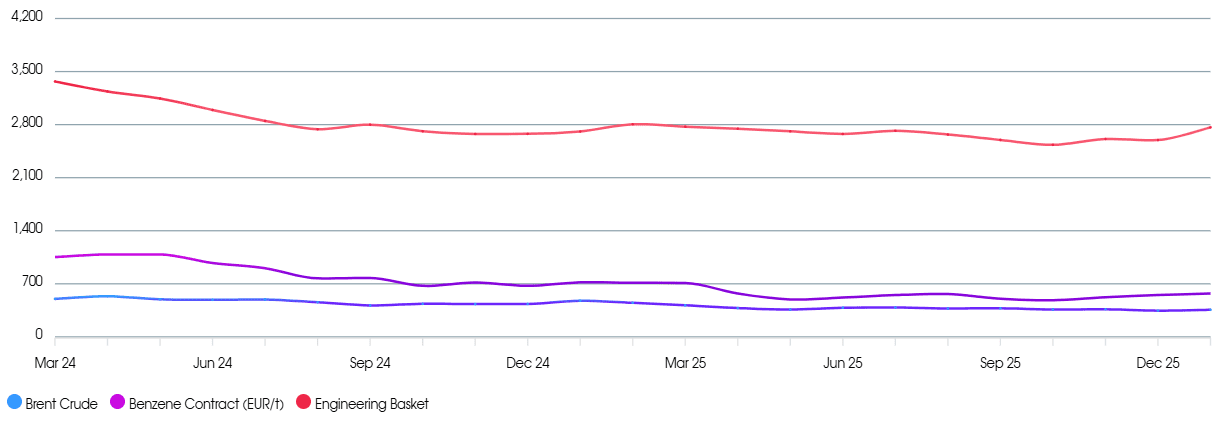

Benzene prices are now at the highest level in nearly a year, with February settling at €790/t, up €130/t from January. The increase was due to the rise in oil prices.

Sustainable Polymers

Recycled Polyolefins have seen very modest increases on the back of the prime market shifting up a little.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE has seen modest increases in February as virgin LDPE is a little tight and this has reopened opportunities for recycled in some applications.

Recycled HDPE

Recycled HDPE has risen a little in February, following the trend in Prime. HD Injection is particularly sought after, especially for easily coloured grades. Quality BM grades are still in demand but some way off the peak of recent years

Recycled PP

Recycled PP is increasing slightly or rolling over, depending on the starting point and the quality of the grade. Demand is up a little but it remains a challenging market.

Price Know-How: February 2026 Full Report

Visit the Price Know-How website to read the February 2026 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.

+44 (0) 1530 560560

Website

Email