Plastribution’s Polymer Price Know-How: May 2026

|

Getting your Trinity Audio player ready...

|

In the May Price Know‑How, Plastribution reports a market settling after April’s buying frenzy, with some standard polymers seeing minor corrections as availability fears ease. Discounted volumes released into Europe have distorted the usual supply–demand signals, yet with Brent Crude forecast to remain above $100 per barrel through 2026, a return to early‑year pricing looks increasingly unlikely. While standard polymers appear to be plateauing, inflationary pressures and falling market prices are squeezing margins for producers of Engineering Plastics, prompting fresh rounds of increases.

The buying frenzy in April, which resulted from availability concerns following the US/Iran conflict and the closure of the vital Strait of Hormuz shipping route, may have resulted in the price of some standard polymers overshooting, and as a consequence, there have been some minor pricing corrections in May.

It is notable that significant quantities of product were released onto the market, often at discounted prices, probably based upon material that was produced and purchased prior to the recent crisis. These additional volumes serve to further confuse the fundamentals of the market in terms of supply and demand, and, in any case, given that Brent Crude Oil is forecast to trade above $100 per barrel for the rest of 2026, then it will be difficult to envisage polymer prices returning to the levels seen at the beginning of this year. A more likely scenario is that prices will plateau, possibly around the current levels for standard polymers.

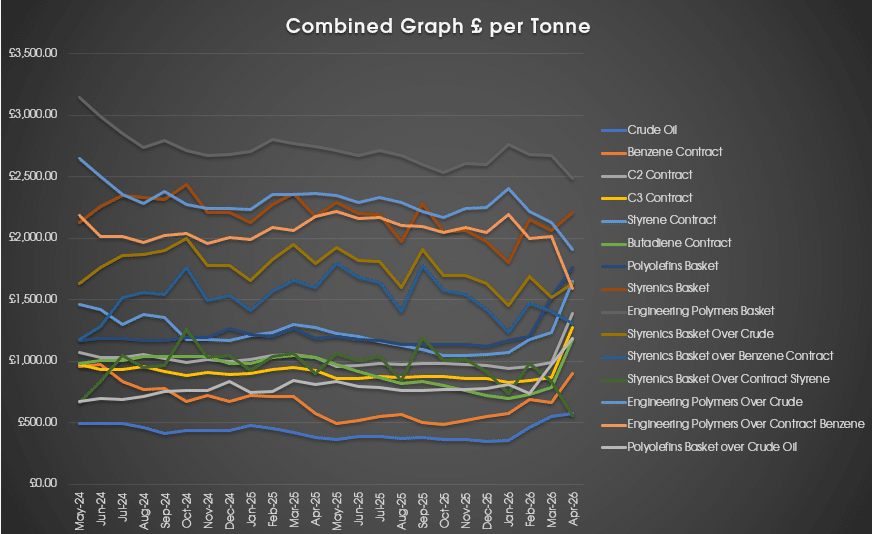

As depicted in the graph below, inflationary pressures in the form of input costs, along with a downward trend in market prices for many polymer types, are eroding the profit margins for producers of Engineering Plastics. Although demand for consumer durables, which constitute a dominant area of demand for these materials, will be stifled by the geopolitical uncertainty resulting from the conflict in the Middle East, producers are already starting to announce significant price increases in an effort to recover profitability.

Whilst a resolution to the conflict would be a welcome relief to many, it is notable that supply chain disruption of which is more likely to come, may last well into the rest of 2026 and possibly beyond. Although not entirely desirable, it is better to have an expensive polymer rather than no polymer at all.

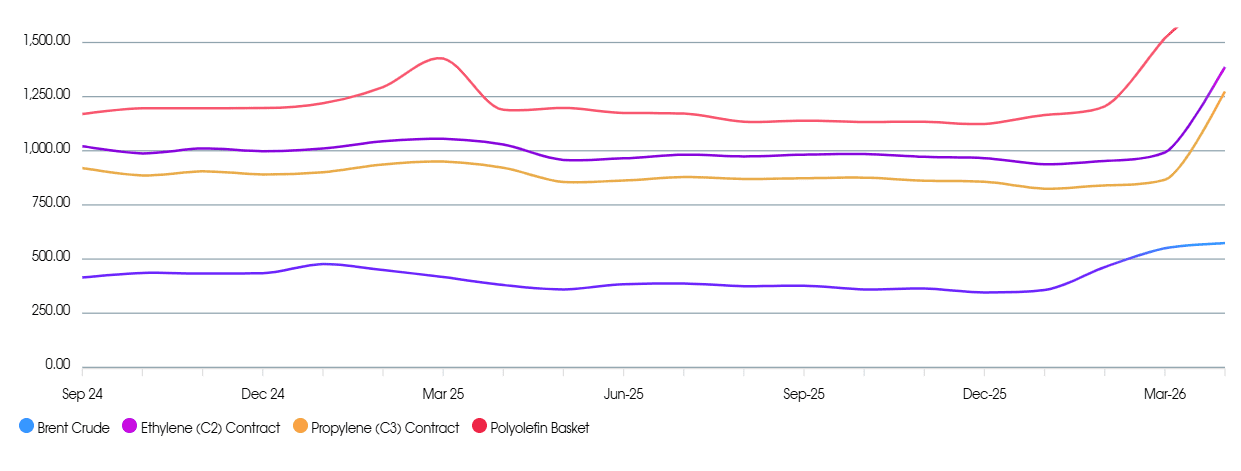

Monomer Price Movement

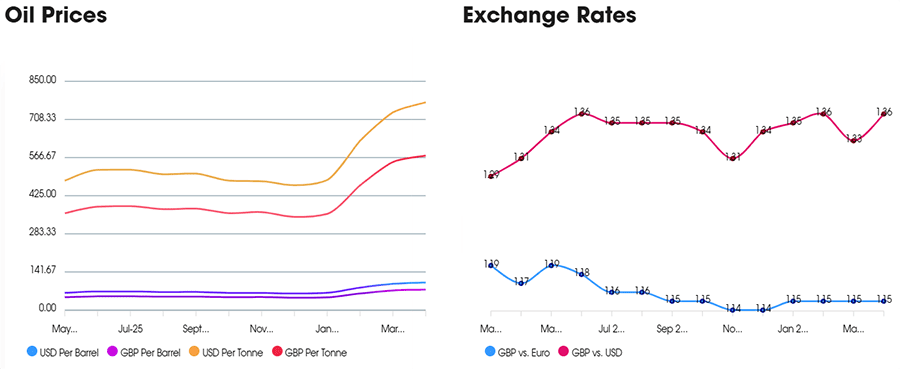

Exchange Rates

€ – 1.15

$ – 1.36

€/$ – 1.18

Standard Polymers

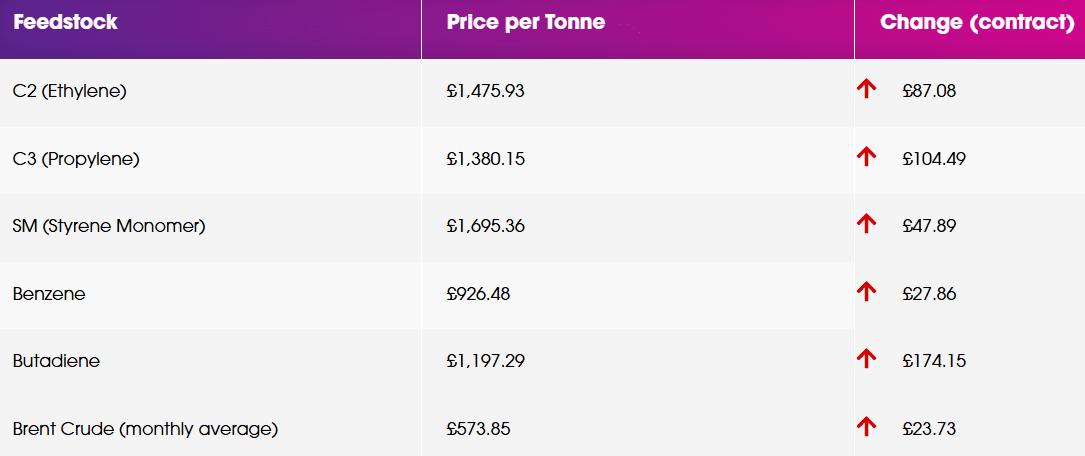

May has seen prices broadly flat with some European producers still pushing for increases reflecting the monomer movement whilst some more import dependent grades are seeing slight reductions. C2 and C3 rose by €100 and €120 / MT respectively and whilst some PP is seeing that passed through, the PE market looks more balanced and the increases way beyond monomer in April have impacted demand.

Whilst imports from the Middle East continue to be severely restricted, we are seeing US imports of PE replace them, but PP is more difficult to substitute and that is keeping prices up

Styrene Monomer is up €55 / MT over April, and the market is passing that through. Availability is restricted, particularly on HIPS with FM in place at Trinseo.

Outlook beyond May is for relative stability, whilst price reductions are welcome, we are unlikely to see anything significant to offset the April increases for some time. We are still seeing shortages on all grades and major challenges in getting product out of the Middle East. We are starting to see the impact of a lack of raw material heading to SE Asia.

There is some expectation that raw material costs will drop in the summer as we hopefully see the coflict resolved and oil prices drop but it continues to be a volatile situation.

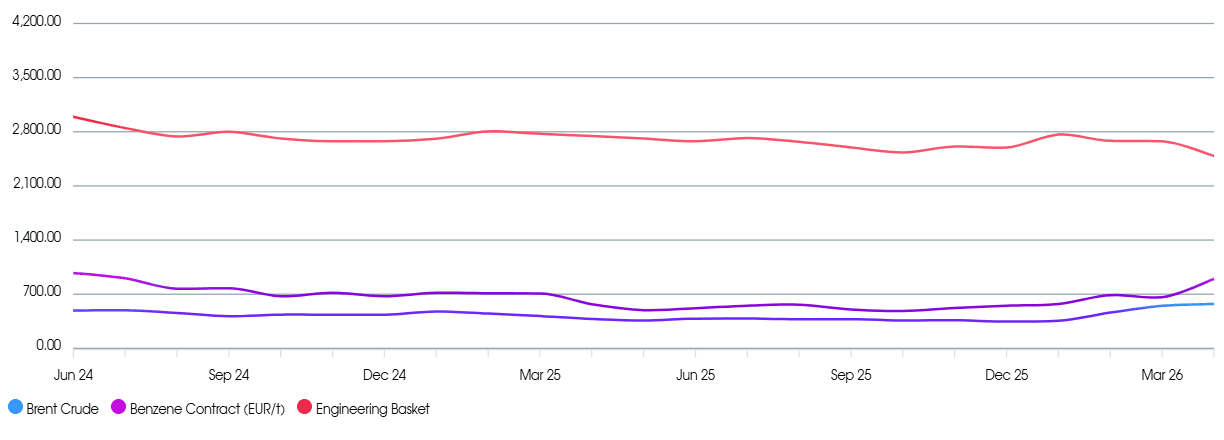

Performance Polymers

The market for performance polymers is still being dominated by events in the Middle East, particularly how it is affecting global supply chains. It remains to be seen just how much of a medium to long term impact it will have, but for now, the messaging is one of higher prices, longer lead-times, and continued shipping issues. With prices still rising in most cases, it looks likely that any stability is still some way off.

The Benzene contract price for May settled at €1064/t, up by a further €32/t from April, with availability also still impacted.

Sustainable Polymers

Recycled Polyolefins are continuing to rise in price, although the pace of increase is softening. As prime prices have corrected slightly down following the boom in April, the momentum has been lost a little bit. Availability of prime is still a concern so we should continue to see better demand for recycled grades and prices holding up. Remains to be seen what happens with new bale input pricing.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE has seen further increases in May though not as strongly as in April. High quality “natural” grades are doing very well with demand now outstripping supply as buyers look for alternatives to €2,400 / MT prime LDPE. Whilst up, industrial grades are not increasing as strongly as supply and demand remain more balanced.

Recycled HDPE

Recycled HDPE continues to climb in price though not quite as strongly as we saw in April. Grades suitable for virgin substitution are in strong demand are trading at similar prices to virgin. More industrial grades are also in demand but supply remains strong and increases are more moderate.

Recycled PP

Recycled PP is up, natural grades for consumer packaging are close to virgin prices. Industrial grades for construction applications etc. are up though the picture is a little more balanced in supply and demand.

Price Know-How: May 2026 Full Report

Visit the Price Know-How website to read the May 2026 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.

+44 (0) 1530 560560

Website

Email